|

So the original article was Money Lessons Grandparents can teach their Grandkids, but I think these lessons are still applicable for parents to pass on to their children.

For ages 3 to 8, the Gift of Delayed Gratification - get them to start saving. My boys are this age. And they love to put coins in their piggy banks. I might get mason jars just so they can see it grow. For ages 8 to 14, the Gift of Hard Work - start giving them paid chores or making them ask neighbours, relatives, family friends for paid work around the house. And when they enter their teens, maybe consider a small business (i.e. baby sitting, pet sitting). For ages 10+, the Gift of Investing - Teach them about investing in the stock market. Open trading account in your name, but solely for stocks that you buy for them or that they want to buy. Review the stocks every so often. Read the annual reports with them. For ages 14+, the Gift of Avoiding Bad Debt - Teach them to stay away from racking up debts for consumption. For ages 17+, the Gift of Saving and Compounding- Encourage them to put away a portion of their pay into savings (i.e. forced savings). Also explain to them how topping up their CPF may not be a bad idea if they have extra money. Often, we talk about leaving a legacy to our children and grandchildren. All the money in the world will not help them if we do not give them the gifts of proper money management. That is a far more important legacy than just cold hard cash.

0 Comments

So it seems there are 15 mentalities that make multi-millionaires stand out. The list is long, so here's my summary of the article:

There are 2 very basic math ideas that really we should know as we make our money plan. If you're a seasoned investor, then there is no need to keep reading this. The first is compound interest. It is one of the most powerful ideas in investing. The formula is: P [(1 + i)n – 1] (P = Principal, i = nominal annual interest rate in percentage terms, and n = number of compounding periods.) If you want to know how it works, let's just take a look at a simple CPF example: Joe is 25 this year and he make $2,500 a month. Assuming that he does not get a pay increase his monthly contribution to his CPF accounts is $500/ month and his employer will pay $425/ month. Where his money goes gets a little tricky.

Now let's assume he also puts $925 in a bank account paying 1% per year. I also excluded the extra 1% the first $60,000 earns in your CPF accounts. There is also no draw down from either accounts. And that the interest rates for CPF (2.5% for OA, 4% for SA and Medisave) and the bank remain the same.

Based on my rough calculations, the difference is $167,362. That's actually quite significant. If we just ran a simple simulation over 30 years where we put aside $100 a month:

As can be seen, a few percentage points can make a huge difference. A 1.5% difference increases interest by nearly 200%. And a 3% difference leads to 460% increase in interest. At 1%, the interest earned makes up about 14% of the total sum earned, at 2.5% the interest earned makes up 33% of the total sum. At 4% the interest earned makes up 48% of the total sum. That's the power of compounding. AsThe next is the Rule of 72. It's related to compound interest. It's basically: 72/i (i= compound annual interest rate as a whole number so 10 and not 0.1 if it's 10%) So basically if you had 10,000 today and managed to grow it by 6% a year, it will take 12 years to double. So in year 12 it will be about $20,000, and at year 24 it will be about $40,000, and $80,000 in year 36. Assuming you did not top up each year.

Just understanding these two simple mathematical formulas can really inform our investing. We have not even introduced the concept of inflation affecting the total sum. Again if we had extra cash lying around, it may not be a bad idea to top up our CPF account if we have not hit the cap, because getting 2.5% returns and 4% returns on a consistent basis is not as easy as it sounds. And it's capital secure.

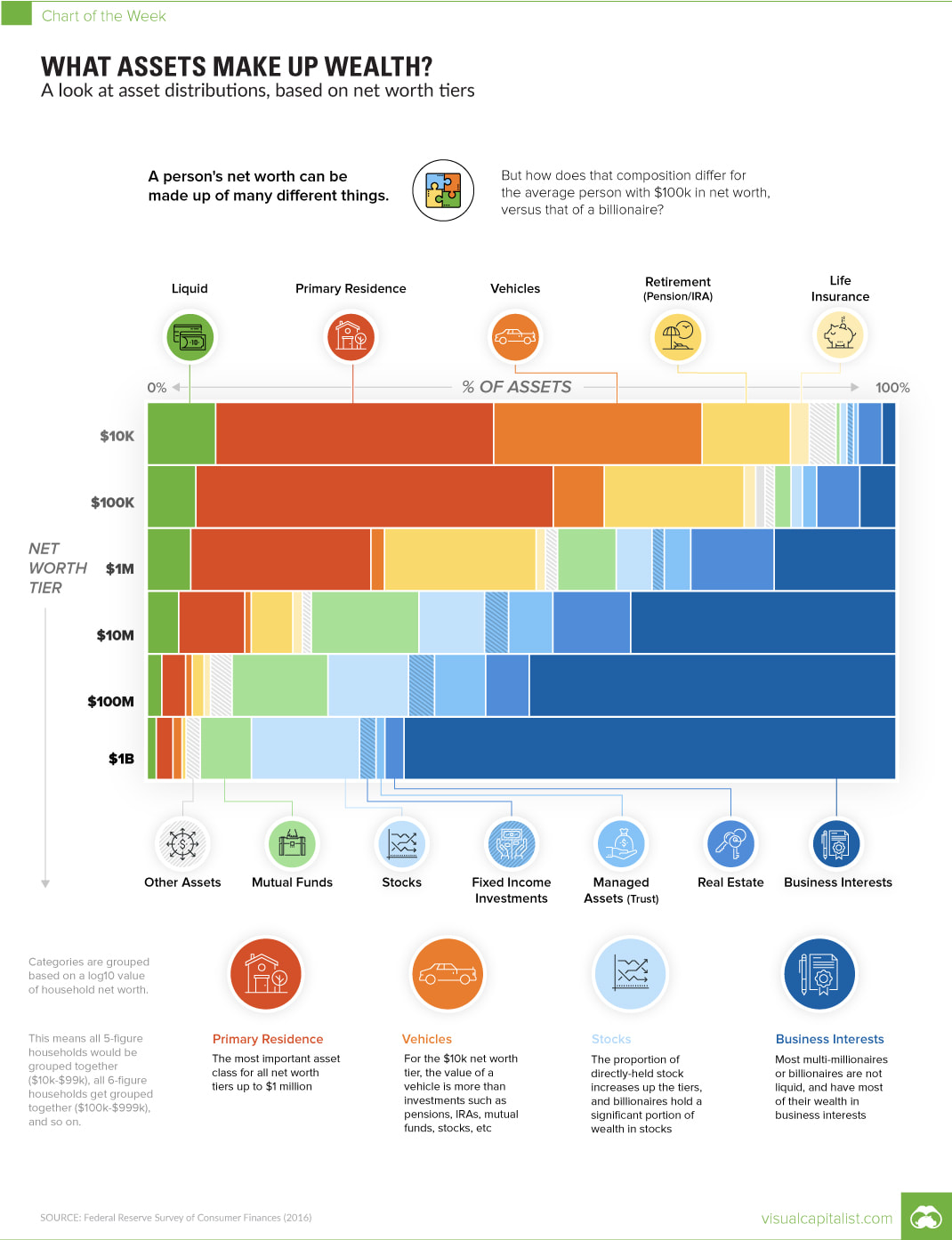

I hope this helps and has not over-math-ed everyone.  Taken from the Visual Capitalist This is interesting.

For folks who are worth more than $100 million and $1 billion have more than 50% of their holdings in business interests. Also, when they past the $1 million mark their primary residence as a share of their holdings go down. Also Real estate investments and even stocks, fixed income investments, and managed assets don't make up much of any brackets wealth holdings. It seems if we want to cross the $100 million mark, we will need business interests.

(Inspiration source) Lots of investing gurus have all sorts of techniques on picking winning stocks, dream portfolios and so on. However, I just read an article about achieving success through sheer exhaustion of all options.

It's like brute force computing. No finesse. No sexy algorithms. The author recommends the following:

It's really interesting. Because it solves all the headaches about trying to pick amazing stocks and having amazing returns. And it might just work. Definitely something to think over. I grew up around the family business, having hung around my parents in their office was interesting. I was playing with typewriters, chops, photocopying machines and the like since I was young. I would listen in on conversations about their projects and how they dealt with problems.

Alas, I became a salary man. I have my reasons. But there are they I wish I could bring my kids in to watch me work. It seems that the best way to build business sense into our children, other than asking them to help you out, is to get them to run their own business. By having a stake in a business they pick up these skills:

I'm not sure what businesses my 4 year olds could run by themselves right now, but this is something I shall keep broaching with them. They are beginning to understand the concept of money, but it's normally "Daddy. Give me money." I've been trying to work into our conversations the idea that they will have to earn their keep. One of them really wants to play golf and he keeps telling me that he wants to play everyday. So I told him he has get a job that allows him to play golf or to turn golf into a job (i.e. go professional). I explained that he has to practice everyday and never give up. Hopefully as they grow we can have more money conversations and to have to figure out how they can make extra pocket money as they are growing up. Textio did an analysis of tech companies' job listings and found that the words that they used reflected what they truly valued.  Similarly, in our everyday conversation our choice of words betray our values. A simple example is: Foreign Domestic Worker, Helper, Maid, Aunty. Each one of these words carry with them certain values of the speaker.

The old saying about pessimists and optimists seeing the glass "half empty" and "half full" is another classic example of how the choice of word betray our values. I take note of the words that people use when describing things, because it gives me an insight into how they think and how they view the world. Similarly, I choose my words carefully when I'm not with close friends or associates. I try to explain more as well giving rise to some folks saying I am "lor sor" (long winded). To re-purpose an old phrase... "Loose Lips Sink Ships". Our choice of words if not carefully chosen ("loose lips") can lead to offending people because from our words they infer certain values ("sink ships"). So we should choose our words carefully. They may betray us more than we know. Disclaimer: This is entirely my own opinion, and I am not a trained financial consultant/ adviser. If you want me to recommend you one, I have some friends who would love to render professional financial advice. Just recently a friend of mine asked me what to do with his CPF OA monies. Should he invest it. Short answer: Maybe. We are going to assume we already have a CPF Investment Account. Things we should consider first before we even think about investing it:

If we answered "Yes" to one or both questions, then the answer is "Don't invest your OA". So if our OA is untouched and unused and we want to be more involved in how our CPF money is used, consider this:

If anyone answered "Yes", my follow up question is "Can I put my money with you as well?" Here's why: The CPF SA is currently at 4% (ignoring the extra 1% on the first $60,000 in all our CPF accounts). That's 4% guaranteed, and we don't even have to do anything at all. We don't even have to think about it. Just transfer your OA to your SA and wait until you retire and get CPF Life. Before we begin, let me just say that if we have spare cash we should be using our cash instead of our CPF money. The reason is that at best our cash earns less than 2% sitting in a bank. Money in our OA gets 2.5%. Everything below can be had by paying cash. So why not use cash first. Once we've used all the cash up then we can consider using CPF money. But let's say we want to get more than 4% returns. Well CPFIS let's us buy certain financial products. We can use our CPF money to buy annuities and/or endowment policies. I won't go into an explanation on what they are. I'm not a fan of endowment plans in general. And, honestly, CPF Life is a pretty good annuity. Might as well pump the amount needed for the Enhanced Retirement Sum from your OA into your SA instead of buying another annuity first. We can still earn the 4% interest while we wait. Next is Investment Linked Policies (ILPs). We can buy ILPs from various companies. CPF Board is so nice that they even created a list for us showing performance of the various approved ILPs. Don't even need to do work. The 2 basic information I look out for are (1) annualised returns over 10 years (or 5 if they don't have 10), and (2) Sharpe ratio. For the annualised returns, I usually check Morningstar (I prefer their layout), but I hear Fundsupermart is just as good. Although CPF Board's 3 year annualised returns may actually take into account returns after fee deductions (because their returns are different, usually lower, from Morningstar). For Sharpe Ratio, CPF Board's calculations are good because they use the OA's 2.5% as a measurement. But if you want to use 4% as the Risk-Free Rate of Return, then you'll have to use a calculator yourself to get the Sharpe Ratio. I think a Sharpe Ratio of 0.75 is pretty ok, considering Warren Buffett's Sharpe Ratio is 0.76. Anything above 1 is good. For example, I'm looking at a China fund, and I am looking at (based on data by CPF Board):

Looking at the available funds, I would be inclined to go with AIA, Prudential or Tokio Marine. Their returns are high, Sharpe Ratio is good. Expense Ratio is high, but so are the others. If that's a key concern (because it eats into your returns) then Tokio Marine is the choice.

The principles for picking Unit Trusts (UTs) is the same as those with ILPs. helpfully, CPF Board also has a list of UTs and their key information. For Exchange Traded Funds (ETFs), we have essentially 4 to choose from:

None of them have more than a 5% return rate, and poor Sharpe ratios. So better to move your OA money into your SA than buy ETFs. Next up are Shares and REITs. There's a whole list of them that we can buy with our OA (click on "View All CPF Investment Scheme"). I cannot really go into detail about what stocks to pick, as everyone has their own way at share investment. Nonetheless, we have to bear in mind that we need to make more than 4% to justify even buying shares and REITs. Honestly, even professionals can't beat the indexes and if we use the SPDR STI ETF and the Nikko AM ETF as proxies for market returns, they're running at about 4.5%. To beat 4.5% we would need active monitoring to ensure our returns are higher. So if anyone is free to do that and can beat the market, can I put my money with you too? Next are Bonds. For corporate bonds we can check the list, and search bonds. There aren't many. We can also get Singapore government bonds, as well as Singapore Statutory Board bonds (although these Statutory Board bonds have to be listed on the SGX Main Board). While the returns are pretty guaranteed (as is the capital), it must be noted that currently there are no rates that are even near 5%. Might as well put it in our SA. The last thing we could invest in is Fixed Deposits (FDs). The banks that are included are (1) DBS, (2) UOB, (3) OCBC and (4) MayBank. As with bonds, while the capital is generally safe, the interest rates do not even come close to 5%. So better put in your SA. My personal take is that if we're not going to actively manage the money we invest, then avoid shares, and REITs. The current rates for Bonds and FDs don't make them worthwhile. The available ETFs can't really beat the SA interest rate of 4%, so probably not. I would avoid endowments, and only get annuities once my SA has hit the Enhanced Retirement Sum (3 X the Basic Retirement Sum). That leaves UTs and ILPs that we can consider since they do no require daily management (probably an annual or semi-annual adjustment). Even then, if we are getting those that cannot perform at 5% consistently, then we are taking quite a bit of risk to chase 1% more interest. At the back of our mind we need to remember that we have a guaranteed 4% interest "product" known as our SA. Also, one more thing to note about our CPFIS, it is not covered by our CPF nomination but by our will. If we do not have a will, then the law of intestacy will kick in (except for insurance where nominations are made). Also your CPFIS investments and cash are not protected from creditors on your death; it may be used to satisfy your debts. (Inspiration source) |

AuthorLate 30s. Dad. Thinking about life, family, work, and retirement. Sharing those thoughts with others Categories

All

Archives

May 2018

|

RSS Feed

RSS Feed