|

Regardless of our life goals and objectives, here are some skills we should develop:

(Inspiration source)

0 Comments

Kiplinger had a great article on fees related to investments.

Here's a simple breakdown of the type of fees to look out for when investing:

Kiplinger just shared their Net Worth Calculator. While it is US specific, it isn't a bad way for us to just get a snapshot of what our net worth is.

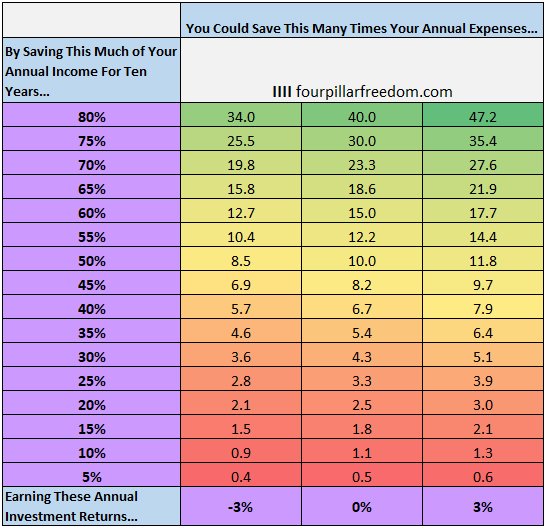

So head on over and find out how much you are worth. In the past, I've talked about using financial brute force and saving your way to retirement. Well Four Pillar Freedom did a test on whether a high rate of savings can offset investment losses. The short answer is yes.  Even at -3% per annum, if you save 50% of your annual income over 10 years, you will have 8.5 times your annual expenditure. Of course, if you're pulling in 3% per annum on your investments then you'd be at 11.8 times your annual expenditure.

What this highlights is that having a high rate of savings is just as important as knowing all the right investment moves to make. The wisdom of an earlier generation of just brute force savings should not be looked down upon or scoffed at. Sure my grandparents may not know much about fancy investment terms like, Alpha or Sharpe Ratio, but they did understand that the more you saved while you worked meant the more you had when you stopped working. Nothing beats simple logic. Sometimes it can feel a little intimidating when we try to get our finances in order. I recommend this step-by-step plan to try and get a handle on our finances:

The plan is not the only one, but it seems logical to me. It also breaks down what seems like an impossible task into bite-sized more manageable tasks. Have hope and give it a go. Let me know if it can be tweaked to make it better. Here are some important questions we should ask when planning our life decisions:

These questions will set the big plans and inform our day-to-day decisions as well. So take some time to answer them. It really doesn't matter how old we are. We can always ask these questions and review them as well. So there's been a lot of complaints about the co-pay required with Integrated Plans (IP).

I get the rationale that there may be over-consumption of medical services which could lead to escalating costs. I also understand the complaints that it may well be the doctors that are driving the prices higher. I find the suggestion of "no claim discount" a good idea. So if you did not make a claim on your IP, you will get a discount on your premium payment. Personally, we may well move towards what is happening in the US. Health insurers in the US are buying up healthcare providers. It's the best way to reduce costs as the health provider now has an interest in preventing over consumption. Of course it comes with its own set of problems regarding under-treating (i.e. moving to the other end of the spectrum). Perhaps if we bought life insurance from them as well, then there may be an incentive to keep us alive longer. Haha. Not sure the intricacies of that. Right now there's an intermediate step being undertaken by some of our insurers. They have a panel of doctors where you get priority appointments and discounts if you use them. I suppose these doctors have an agreement with the insurers to charge accordingly and not jack up prices. I was thinking that perhaps that the co-payment requirement could only be for those IP that allows the use of private healthcare providers. If you get an IP that only allows for stay at restructured hospitals, then there is no co-payment requirement. I believe that restructured hospitals can be convinced by MOH to keep their costs manageable. If our healthcare costs continue to escalate I foresee our private healthcare providers being slowly gobbled up by the insurers. It may not be a bad thing I suppose. Some tips on having a diversified portfolio

So I know a guy. He's 50ish.

He makes $180,000 per annum and his annual expenditure is $200,000. That sounds bad except for the fact that he's pretty good with his investments. So he collected a dividend of $60,000 in 2017. Now, he has a policy of putting half of the money which he earns from his dividends into his savings account, which he does not touch, except in emergencies. He has had a few dips in the past, but he's never really had to touch his savings. As such, he has accumulated, in his savings account, $800,000 over the years. Now he knows that he's getting older and medical costs are going up, also he still has to support his kids along with his aged parents. He figures that he should find some way to increase his income so as to meet his expected costs going ahead in 5 to 10 years time. So he's tightening his belt a little and trying to trim expenses wherever he can. His friends keep telling him that he doesn't have to be so frugal. He's got a lot of money in the bank, and his investments should more than cover any increase in spending. Instead of putting 50% in savings, why not put 40% or even 20%. That way he can meet rising expenses. He can even dip into his savings. Some friends are even suggesting he sell off some of his properties also. With all that money, maybe he can even live a little. Does this sound familiar? If Singapore were a person, it would be something like that. Of course as a person, trying to get a higher paying job is one way to increase income. For a country, the best way to raise income is to raise taxes. Borrowing money is another way, but it means that you have to pay it back sometime. The reliance on investment income is an illusion, because when markets take a hit, our investments also take a hit. Even if we are long term investors who stay calm and stick to our plan, there could be lean years where dividends are not high and no growth in our stocks. I am very suspicious of people who say we can spend more of our investment income, or to do that and sell off the land (like HK) Makes me think they are not very good with their own money. I wouldn't trust them to manage my funds, later go missing. I'm already not very comfortable with infrastructure funding being financed by borrowing as it may put our debt in foreign hands, needing to borrow more for other expenses does not sit well with me. It's like a guy who keeps borrowing money from the bank to finance all his purchases. It's just accumulating debt. And I'm even more against selling off land, because in HK most of the land is in the hands of the few. Prices are sky high, and the government has no effective way to pay for stuff except to sell off even more land (it's not that don't want have GST, they don't have the political balls to do it). So they merrily sell off their land, and I'm just waiting until they have none left to sell. Then essentially they will all be in the thrall of the tycoons, and, indirectly, Beijing. So much for their democracy. So if you think about our country's budget plans as if it were a personal budgeting plan, it is a very sound plan for the medium to long term. And I'm not the only one. There's a lot to consider if we have a large amount of wealth to handover to our kids.

One common way is that we just don't tell our kids what we have and what they will be inheriting. Ultimately that leaves the kids in the dark, and makes it difficult for them to decide how to structure their lives. Either they try to go fully independent and try to structure their lives as if there is no financial support from us, or they continually ask for additional support, especially if they have kids. This can become awkward when it comes to asking for money and so on. Another common way is to set up a trust to have the money distributed to the kids after we have passed. However, this only meets the parents' interests and not that of the kids. Mine are still young, but I have to remember that when I pass they'll be adults too (hopefully). We hope that we would have raised financially responsible kids. If that's the case then why lock it into a trust, since they are fully capable of managing the money. And if they are financially irresponsible, a considerable amount of their energies will go to unlocking the trust and/or challenging the will. Also, we have to remember that our grandkids or great grandkids will inherit the money (trusts cannot last longer than 100 years in Singapore, unless a charity trust). If our kids didn't pass on good money habits, our "protection" only lasts one or two generations after us. Thus fulfilling the 富不过三代 saying. My personal take is that as a family, we should sit down with our children, be honest about what we have, and discuss what the family goal is. I believe that having a common family mission will ensure that the throughout the generations the wealth will be preserved for that purpose. Money for money's sake is not really a uniting mission. But a family deciding that the wealth should be used to support education, welfare, health or the arts, or to ensure the family business becomes the market leader/retain market position (other than supporting members of the family), will mean that the family has a mission. The mission will keep various members on track and allow them to structure their lives. It means that the wealth may survive beyond the 3rd generation as each generation passes on the family mission. (Inspiration Source) |

AuthorLate 30s. Dad. Thinking about life, family, work, and retirement. Sharing those thoughts with others Categories

All

Archives

May 2018

|

RSS Feed

RSS Feed